Introduction

Psychology of Money is probably one of the most popular books in recent times around the personal financing space. The book’s primary focus is not so much on how to invest money or how to invest money rather it is on how we think and behave fundamentally about money.

It is a book by Morgan Housel that explores the psychological biases and irrational behaviors that drive our financial decisions. The book argues that while money is a tool, it is often treated as a goal in and of itself, leading to poor decision-making and a lack of fulfillment.

Here is a quick summary and some key takeaways from the book:

Psychology of Money Summary | The Psychology of Money Summary

Protect Capital

Many people become rich but then they also end up losing all of it very soon there are so many such examples we can see in history that’s why it’s very important to constantly protect your wealth. The primary focus of investing should be avoiding bad decisions.

Give equal importance to wealth protection which you usually give to generating wealth. It is necessary to take risks but it’s equally important to preserve capital. Building wealth has little to do with your income or investment returns but a lot to do with your savings rate.

There is a lot of uncertainty and risk in the first two. But saving is the only factor that you control. You can build wealth without a high income, but there is no way you can build wealth without a high savings rate.

Financial Independence

This is the central theme for most of the personal financing books however it is imperative to mention it here as it would not be complete without this. Money should be used to gain financial independence “You will be truly wealthy if you use your money to buy time” When you can do whatever you want, whenever you want, and for as long as you want you will be truly financially independent.

Being wealthy vs Being Rich

Another key takeaway is that real wealth is not what is seen but what we do not see. The only difference between being wealthy and being rich is that it is not difficult to recognize rich people because they own luxury cars and expensive houses. Even if they have bought it on EMIs.

In our society, people judge your wealth by your spending ability. But wealthy people do not spend most of their income. Their real wealth is in the form of assets such as stocks, rental income, intellectual property, etc. Wealthy people use their money to grow themselves and to give themselves greater flexibility and the ability to make choices.

Always have a Plan B

The fourth learning is that we should always be ready for surprises and unknown events and keep a plan B ready. In fact, start from Plan B before you go to Plan A. We must accept the randomness and uncertainty in life and plan for it.

For this, we have to solve the difference between two things- What is about to happen and What could happen? Often we take all the decisions thinking about what is going to happen according to us and do not think about what could happen, and if it happened, then how we would be able to face the situation.

Also Read: Book Summary Think and Grow Rich

The reason for this is that we always think that we should know what is going to happen in the future. It is very difficult for us to admit that we do not know much about what will happen tomorrow, and therefore, we should be prepared for uncertain events.

There are no free lunches

Another great learning that applies to all aspects of life rather is that there are no free lunches. For example, social media handles are free but in reality, they are asking for your time and data instead of money. Therefore, everything has a price.

We should know what that price is, and then decide whether we want to pay it or not. Similarly, if we talk about investment, we also have to pay a price that you cannot measure in dollars or rupees. The real price of investing is to deal with various emotional and mental states like fear, doubt, uncertainty, greed, and regret.

According to Morgan Housel, instead of being afraid of market volatility, we need to think of it as a fee or a cost that one needs to pay to become a good investor. In investing, until we deal with emotions and invest rationally, we will not be able to be good investors.

Money is a tool, not a goal

The pursuit of money for its own sake can lead to poor decision-making and a lack of fulfillment. It’s important to have financial goals, but they should be tied to the things we value most in life, like relationships, health, and personal growth.

Learn to control emotions

We are influenced by emotions and social norms. Our financial decisions are often influenced by our emotions, such as fear, greed, and envy, as well as social norms and peer pressure. It’s important to be aware of these biases and try to make decisions based on logic and long-term goals rather than short-term emotions.

Power of Compound Interest

Compound interest is the process by which the interest earned on an investment is reinvested, leading to exponential growth over time. Many people underestimate the power of compound interest and the importance of starting to save and invest early in life.

Short Term Focus

We have a tendency to focus on the short term. We often prioritize immediate gratification over long-term planning, leading to poor financial decisions. It’s important to think about the long-term consequences of our financial choices and to have a plan for the future.

The Psychology of Money Chapter | psychology of money chapter 1

The Psychology of Money book is divided into the following chapters:

- The Anchor: how we use the past to make sense of the present and the future

- The Compound: how small, smart decisions can lead to incredible success or failure

- The Story: how our beliefs about money shape our behavior

- The Finite: how our brains handle scarcity and abundance

- The Emotions: how our feelings about money drive our behavior

- The Social: how our relationships with others influence our financial decisions

- The Ego: how our sense of self shapes our financial behavior

- The Identity: how our financial decisions reflect and shape our sense of self

- The Risk: how our tolerance for risk affects our financial choices

- The Resilience: how our ability to adapt to change shapes our financial success

Each chapter in the psychology of money book explores different psychological biases and behaviors that can influence our financial decision-making and offers insights and strategies for improving our financial well-being.

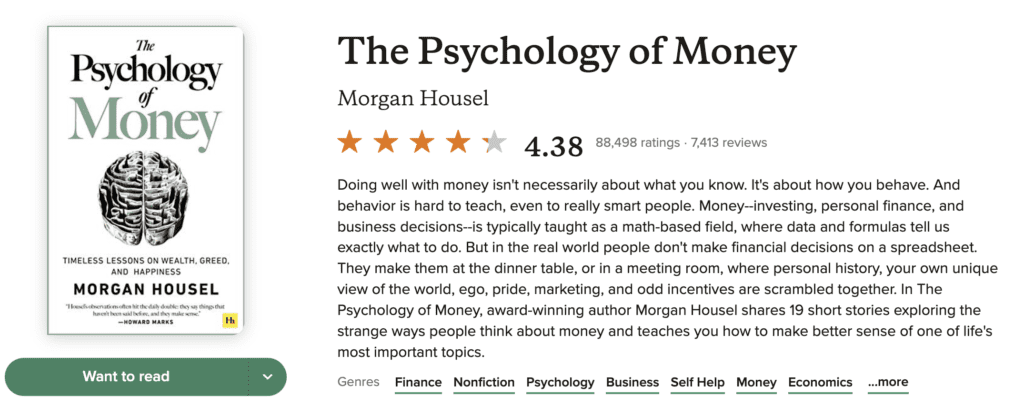

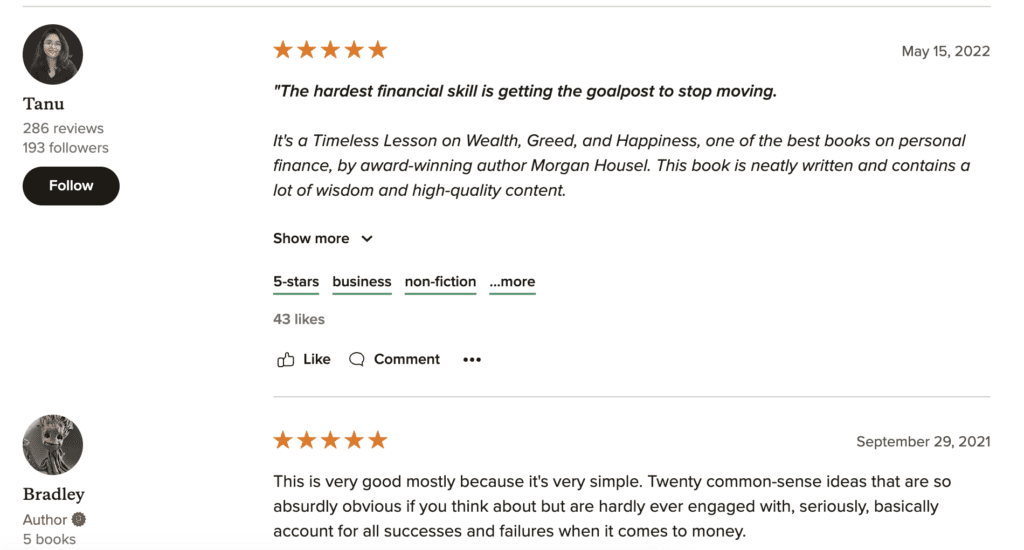

The Psychology of Money Review

The Psychology of Money by Morgan Housel is a thought-provoking and engaging book that offers a fresh perspective on the psychological factors that drive our financial decisions. The book is well-written and easy to understand, making it accessible to readers from all backgrounds and levels of financial knowledge.

It is an excellent resource for anyone looking to improve their financial well-being and better understand the psychological factors that drive their financial decisions. It offers a unique and valuable perspective on personal finance and is highly recommended for anyone interested in improving their financial literacy.

It has received rave reviews all over the internet.

Here are some of the reviews from goodreads.com about the psychology of money.

Books similar to the psychology of money | psychology of money book

Here are a few books that are similar to The Psychology of Money and explore the psychological biases and behaviors that influence our financial decision-making:

- Thinking, Fast and Slow by Daniel Kahneman: This book delves into the psychological biases that influence our thinking and decision-making, including those related to money.

- Your Money or Your Life by Vicki Robin: This book is focused on personal finance and offers practical advice for improving financial well-being. It emphasizes the importance of aligning your financial goals with your values and priorities.

- The Intelligent Investor by Benjamin Graham: This classic book on investing offers a framework for making informed and rational investment decisions. It emphasizes the importance of understanding and managing risk.

- Rich Dad Poor Dad by Robert Kiyosaki: This book explores the different approaches to money and financial literacy taken by the author’s two fathers. It offers practical advice for building wealth and achieving financial independence.

- The Total Money Makeover by Dave Ramsey: This book is a step-by-step guide to improving financial well-being and achieving financial freedom. It offers practical advice on budgeting, saving, and investing.

ALSO READ: 5 must-read books for every investor

Psychology of money quotes

The psychology of money pdf | psychology of money book pdf

I would strongly argue that you add the psychology of money pdf copy to your collection of books if you like the digital form of reading. If you have a kindle then kindly get a copy from amazon below and add it to your kindle collection forever. I can assure you that this would be the best investment you will ever make in a book.

Psychology of money audiobook

If you are into audiobooks then this is a must-have book to add to your collection. Listen to it on a long walk or drive.

Final Thoughts

To conclude, the Psychology of Money highlights the psychological biases and irrational behaviors that can influence our financial decisions. By being aware of these biases and making an effort to make logical, long-term financial choices, we can improve our financial well-being and achieve our financial goals.

If you have already read this book then share your feedback in the comments section. If you have any questions kindly contact us or send inquiries to contact@investing20.com.

1 thought on “The Psychology of Money Summary”